Happy 2026! We are kicking off the year with updates from Europe and California.

In Europe, after almost a year of negotiations, Omnibus talks concluded with revised reporting thresholds and exemptions for in-scope companies. Separately, EFRAG submitted its Simplified ESRS recommendations to the European Commission, giving companies the tools to begin re-assessing their CSRD reporting strategy.

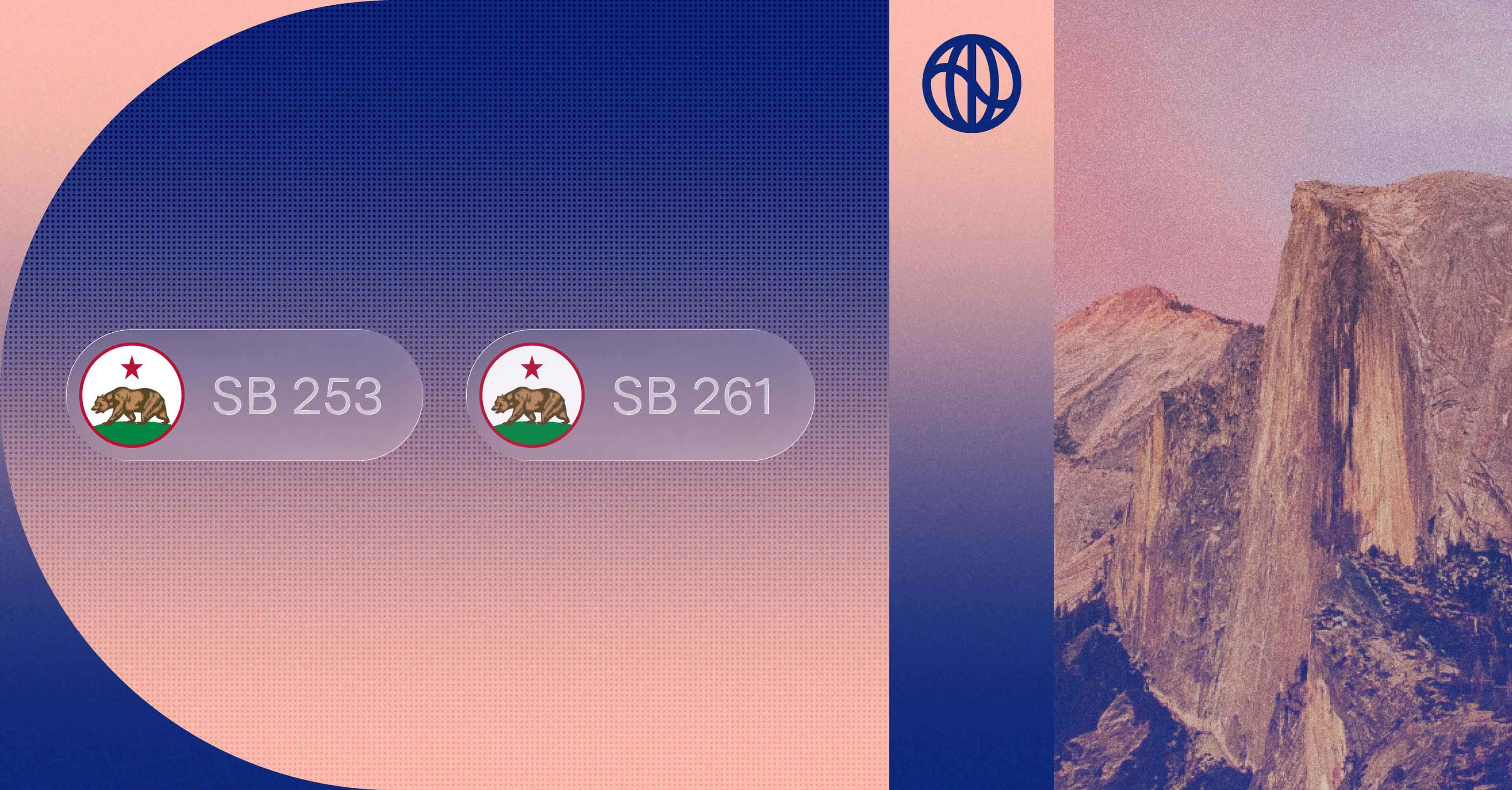

In California, the Ninth Circuit Court of Appeals heard arguments in the US Chamber of Commerce vs. Sanchez case assessing the constitutionality of California’s climate disclosure laws, SB 261 and SB 253.

Below, we break down what companies need to know.

Europe: Omnibus agreement reached; Simplified ESRS submitted to European Commission

Read our full guide to the Omnibus agreement.

December brought long-awaited clarity to European sustainability reporting as the Commission, Parliament, and Council reached agreement on the Omnibus reforms to simplify the CSRD and CSDDD.

Why it matters: The Omnibus agreement includes new reporting thresholds and exemptions for in-scope companies. Approximately 5,000 companies are expected to be in scope under the revised CSRD.

The details:

- New CSRD thresholds for EU companies: €450 million worldwide net turnover and 1,000 employees.

- New CSRD thresholds for non-EU companies: Consolidated EU net turnover ≥ €450 million and at least one EU entity or EU branch with net turnover ≥ €200 million.

- Assurance requirements reduced: Only limited assurance required, with reasonable assurance removed entirely.

- Value chain protection: Companies prohibited from requesting sustainability data from suppliers with fewer than 1,000 employees beyond voluntary ESRS requirements.

Additionally, EFRAG submitted its simplified European Sustainability Reporting Standards (ESRS) to the Commission for adoption. The simplified standards remove over 60% of original data points—mostly qualitative—while retaining most quantitative metrics. Companies can now use estimates for value chain data, and many data points are clarified for better interoperability with ISSB standards.

The Commission aims to adopt the simplified ESRS by mid-2026. Companies already reporting will continue under current ESRS through 2027 (unless future exemptions are provided), with simplified standards mandatory for 2028 reporting on FY2027.

Formal procedures to finalize the revised CSRD are expected to be complete in Q1. Member states will then transpose this into their national laws between 2026-2027, with Wave 2 CSRD reports due in 2028 on FY2027 data.

What to do now: Assess whether you are still in scope for CSRD and review the draft ESRS summary to get a sense of what new requirements could look like.

California: Ninth Circuit hears arguments on California's climate disclosure laws

In November 2025, the Ninth Circuit Court of Appeals temporarily paused enforcement of California’s climate risk disclosure law (SB 261) to review a legal challenge by the US Chamber of Commerce. On January 9, a three-judge panel heard oral arguments on the legality of SB 261 and SB 253.

Key takeaways:

- Laws treated as separate issues. The panel drew clear distinctions legally between SB 261 (climate risk disclosure) and SB 253 (emissions reporting), with the judges differentiating between the narrative-based versus quantitative requirements.

- Decision expected in next few months. Judge Nguyen stated the panel had not yet discussed the case. We expect a written decision between February and April.

- Multiple possible outcomes. The case could go in several different directions. The Court could adopt the lower court’s reasoning and uphold both laws, enjoin one or both laws, or send the case back to the trial judge with instructions on how to sever out problematic sections of either law.

What’s next: In the meantime, companies have continued to draft and publish SB 261 reports, as well as continue to prepare for SB 253 reporting. The deadline for SB 253 (August 10, 2026) remains in effect.